Funding retirement is a priority for many Canadians. For those without a workplace pension, the RRSP often becomes a key tool in building long-term financial security. While the first 60 days of the year tend to bring the most attention, effective RRSP planning is designed to support your goals year-round.

How Much Can You Contribute?

Your RRSP contribution room is generally calculated as:

A. Unused RRSP deduction room carried forward

Plus

B. The lesser of:

❖ 18% of your previous year’s earned income

❖The annual maximum, $32,490 for 2025 and $33,810 for 2026

Less

C. Unused RRSP contributions previously reported

Plus

D. The $2,000 cumulative overcontribution allowance

Your official numbers are confirmed in your CRA Notice of Assessment.

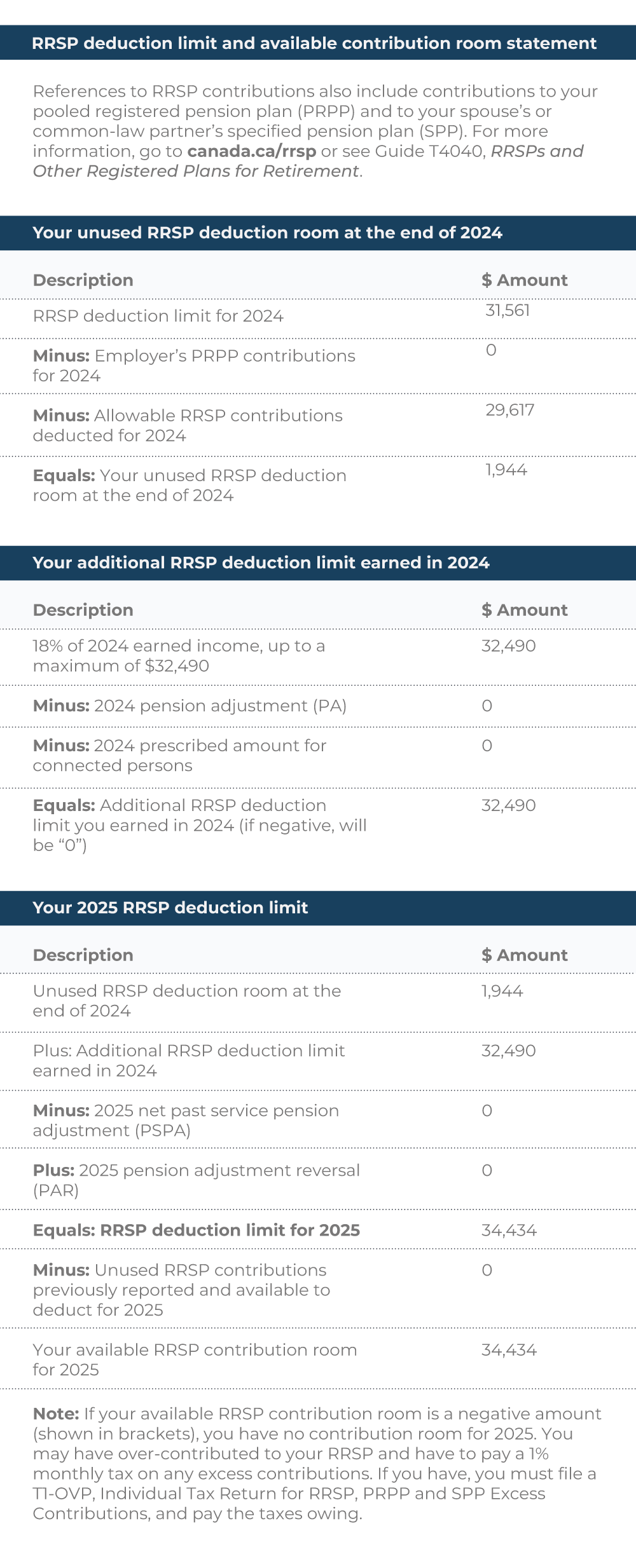

Understanding Your RRSP Statement

After filing your tax return, CRA issues a Notice of Assessment that includes your RRSP Deduction Limit and Available Contribution Room.

For example, if someone had:

❖ $1,944 in unused deduction room

❖ $32,490 in newly earned room

Their total deduction limit would be $34,434.

If they also had $20,000 of unused contributions already reported, their new available contribution room would be reduced accordingly. Understanding this difference can help prevent overcontribution penalties.

Contribution vs. Deduction

An RRSP contribution is the deposit you make.An RRSP deduction is what you choose to claim on your tax return.You may contribute now and defer the deduction to a future year if you expect to be in a higher tax bracket. This flexibility can provide additional tax efficiency when used strategically.Timing MattersContributions made in the first 60 days of the year can generally be applied to the prior tax year or carried forward. Proper timing can help align deductions with your broader income and tax planning strategy.

Additional Planning Considerations

RRSPs may also support:

❖The Home Buyers’ Plan, allowing eligible first-time buyers to withdraw up to $60,000

❖ The Lifelong Learning Plan, allowing up to $10,000 per year, $20,000 total for qualifying education

❖ Spousal RRSP strategies to help balance retirement income

❖ Evaluating whether a TFSA may be more appropriate if funds may be needed within five years

Every situation is different. The right strategy depends on your income today, your future expectations, and your long-term goals.

If you would like support reviewing your RRSP contribution room or planning for 2025 and 2026, connect with MNK Financial Services and we would be happy to guide you through your options.

Disclaimer

Camaco Capital Management is an owner and partner in the Q Wealth Partnership. Portfolio Management services are provided by Q Wealth. Financial planning services are provided by Camaco Capital Management . This document has been provided for information purposes only and is not intended to be relied upon as investment, financial, tax or legal advice. Please consult an independent legal or tax professional if considering the implementation of a planning strategy. The planning strategies and technical content are provided for the general guidance and benefit of our clients at the time of writing; however, we cannot guarantee the accuracy or completeness of the information contained herein.